Provisional tax – Who, what, when, where, how?

Who pays provisional tax?

All companies will be provisional tax payers.

Individuals need to also register for provisional tax if they earn income other than a salary/remuneration, for example rental income from a property, income from a trade or interest from investments. There are two exceptions here:

- If the income earned other than a salary/remuneration is under R30,000 per year.

- If you are under 65 and your total taxable income is less than R83,100, or if you are 65 to below 75 and your taxable income is less than R128,650, or if you are 75 or older and your taxable income is less than R143,850 for the 2021 tax year.

What is provisional tax?

Provisional tax is not a tax separate from income tax, but is rather an advanced payment on the income tax liability of an entity/individual. The idea is that you pay tax provisionally to ensure that you do not end up with a large tax debt when you are assessed.

Where do you submit provisional tax?

On your company’s e-filing profile, you can register for provisional tax, when the time comes, you then generate what is called an IRP6, this is then filled out and submitted. You can then also pay your provisional tax through the e-filing channels.

When do you have to submit provisional tax?

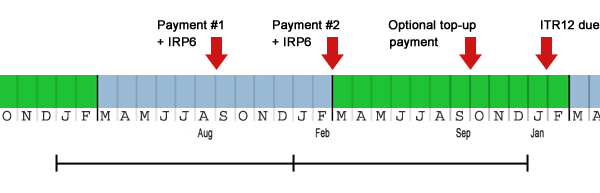

The first provisional tax payment is made 6 months after the previous financial year end. The second provisional tax payment is made on financial year end. The third provisional tax payment is optional and is only paid if the previous two payments were insufficient.

For individuals and entities with a February year end, this is due at the end of September, for all other entities with a year end other than February, this provisional tax payment is due 6 months after year end.

How do you calculate provisional tax?

For the first provisional tax payment you will calculate all the actual income earned and subtract the actual deductions incurred up to the most recent date for which the data is available. You will then estimate the income and expenses/deductions for the remainder of the year. Add the two to get to an estimated taxable income for the year. Now calculate the tax payable on this projected taxable income and halve it, this will be your first provisional tax payable.

For the second provisional tax payment you will calculate all the actual income earned and subtract the actual deductions incurred up to the most recent date for which the data is available. You will then estimate the income and expenses/deductions for the remainder of the year. Add the two to get to an estimated taxable income for the year. Now calculate the tax payable on this projected taxable income and deduct what was paid on the first provisional tax payment, this will be your second provisional tax payment.

As you are working with estimated figures, SARS does allow for a margin of error before they will impose penalties and interest on the underpayment of provisional tax. For individuals and entities with taxable income of under R1,000,000 for the year, you need to make sure that your estimate of taxable income is 90% or more of you actual taxable income, for individuals and entities with a taxable income over R1,000,000 the ratio goes down to 80%.

The third provisional tax payment is due 7 months after year end for individuals and entities with a February year end and 6 months after financial year end for all other entities. This is an optional tax payment and is only done when the individual/entity realizes, now that they have the actual figures in front of them, that they underestimated the provisional tax. This will then be submitted to reduce the risk of paying interest on the underpayment of provisional tax, the penalties will still be levied, but the interest will be curbed.

To avoid penalties and interest altogether, it is best to work with the most accurate data possible and ensure that the estimated taxable income is within the ratio’s given above.

DKS Financial Services can assist you with your provisional tax calculations and submit your returns timeously. Contact us today to discuss your unique requirements.